View

The 1031 exchange is an essential financial strategy for investors, especially within the agricultural industry. Known formally as a "like-kind" exchange, it allows farmers, ranchers, and agricultural landowners to defer capital gains taxes from the sale of one property by reinvesting proceeds into another qualifying property.

Agricultural landowners can significantly benefit from 1031 exchanges. Farmers and ranchers frequently own multiple parcels of land designated for various purposes such as grazing, crop production, or timber harvesting. Selling one parcel and reinvesting in another property of equal or greater value allows investors to:

A 1031 exchange provides crucial tax-deferral benefits. Specifically:

Agricultural properties eligible for 1031 exchanges include:

Investors should collaborate closely with qualified tax advisors to ensure compliance and optimization of the transaction.

If agricultural land includes a primary residence, the property qualifies as mixed-use. In this scenario:

To comply with IRS regulations, property owners must:

Engaging a qualified intermediary is crucial in navigating a 1031 exchange. Intermediaries assist with:

Eligible replacement properties in a 1031 exchange include:

A Delaware Statutory Trust offers an attractive option for investors seeking passive management of high-quality commercial properties. DST benefits include:

DSTs can also serve as backup properties to ensure complete utilization of exchange proceeds.

The agricultural land 1031 exchange is a strategic tax-deferral tool enabling investors to leverage capital gains tax savings, diversify portfolios, and achieve long-term financial growth. By working with qualified intermediaries and exploring options such as DSTs, agricultural landowners can significantly optimize their real estate investments.

As market conditions have improved, we see many investors opting to sell specific current real estate holdings. In some cases, these property sales have high Loan to Value (LTV) ratios that present challenges to investors planning to pay, reduce or defer their capital gains tax. In most cases, there may be strategies to help maximize the investor’s after-tax sale proceeds.

The Investor’s Problem

For investors with a low or no taxable basis, the sale of the relinquished property can create a scenario where the capital gain is higher in proportion to the equity proceeds available for reinvestment or tax liability payment. The higher LTV creates a high level of mortgage boot. It is critical that the investor consults with their tax advisor to calculate and understand the potential tax liability created from the sale.

Illustration 1 demonstrates an example of the high LTV scenario. Based on the assumption of the sale of a $1,000,000 property with a 70% LTV and a remaining basis of $25,000, the investors could end up using a majority of the cash proceeds to cover the potential tax liability.

Potential Solution – Partial Exchange

Strategy to cash out while reducing potential Mortgage Boot and potential total Tax Liability

The investor whose objective is to cash out and maximize the amount of remaining equity proceeds from the sale may consider a strategy to help reduce the high level of mortgage boot and further reduce to overall all potential tax liability.

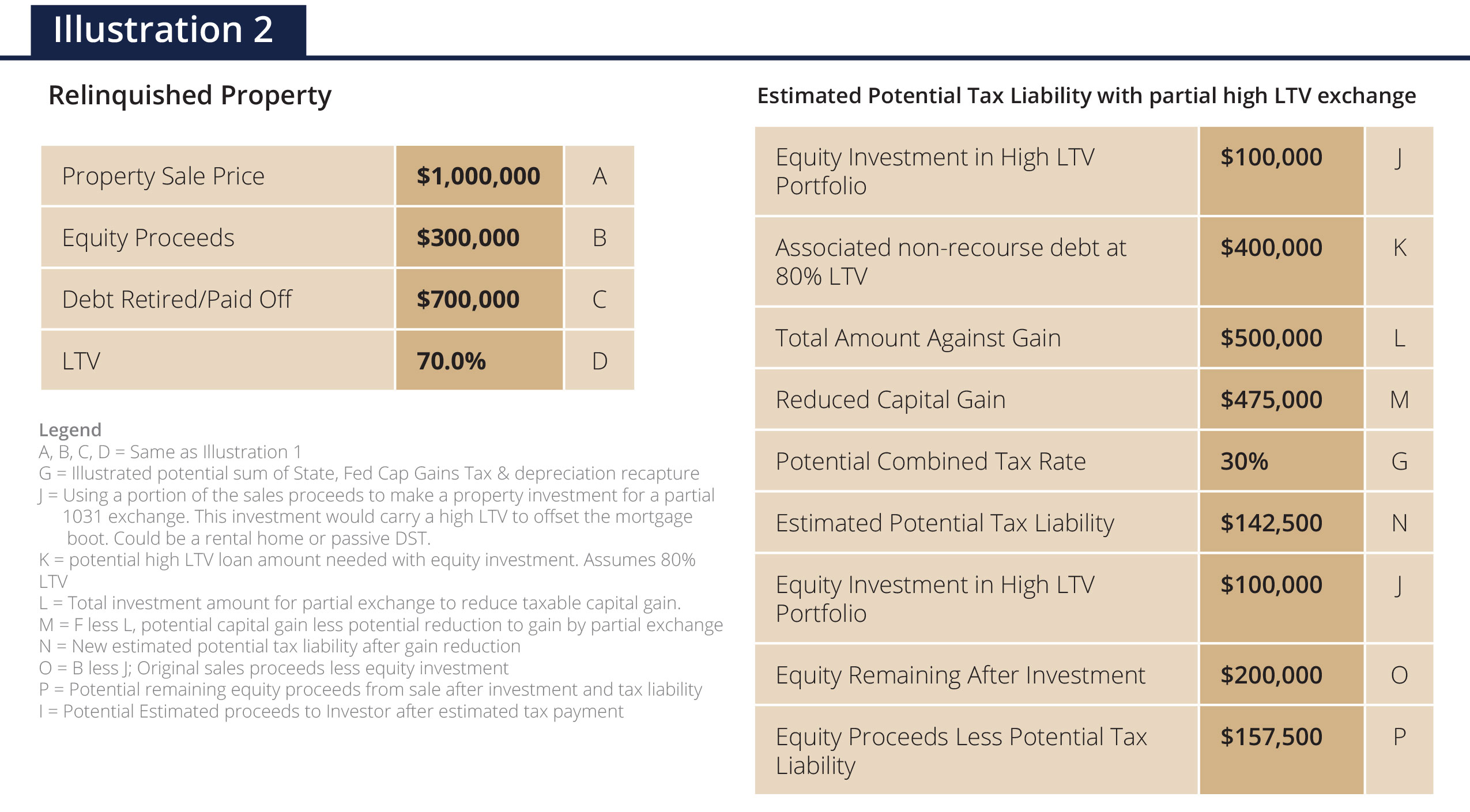

The investor could purchase a like-kind replacement property with a portion of the equity proceeds and a high LTV. This could be a direct property purchase with a high LTV or a DST with a high LTV. Illustration 2 demonstrates this scenario. Our example shows more significant after-tax proceeds than Illustration 1 and has a portion of the funds working for the investor and not paid as tax.

Further, this strategy can also be used in a full exchange with other cash-flow generating properties or DSTs

More information on the High LTV DST

The High Leverage, Zero Coupon DST is a portfolio of properties leased to tenants of excellent credit. A bank is generally willing to lend a high LTV amount with the assumption that the loan will hyper amortize.

All of the tenant’s rents will go to the loan interest and principal and reduce the LTV over the hold period. No cash flow is paid to the investor, but each payment should increase the investors’ equity in the DST.

Opportunities exist in the marketplace for investors to diversify their real estate holdings while deferring capital gains of highly appreciated and long-held assets. Real estate property owners may find utilizing a combination of Section 1031 Exchange and Section 721 Exchange, also referred to as a "Two-Step UPREIT Transaction", to be a beneficial tax mitigation process. Knowing that each investor's specific situation is different, we recommend that the investor seek the advice of tax and legal professionals to understand risks and how this can apply to their unique situation.

Rather than a 1031 like kind exchange, a 721 Transaction allows an investor to contribute property directly to a Real Estate Investment Trust (REIT) operating partnership (the entity through which the REIT acquires and owns its real estate) in exchange for operating partnership units (OP Units). A 721 Transaction may be helpful for property owners with significant gains where a sale would incur a tax liability or those looking for estate planning tools to pass wealth on to heirs in a tax-efficient manner. The most recent year brought concerns around the future of Section 1031, and the 721 Transaction may be an option to diversify away from these uncertainties.

Section 721 of the Internal Revenue Code permits owners of real estate properties to contribute their assets, on a tax-deferred basis, to a partnership in exchange for interest or operating units in the partnership. REITs often hold their real estate portfolio through an operating partnership known as an Umbrella Partnership Real Estate Investment Trust, or UPREIT. The UPREIT structure allows real estate holders to exchange their property for OP Units of the operating partnership by contributing that property through a 721 Transaction. The OP Units have a similar structure to the shares of the REIT and, after a predetermined time, can generally be converted to actual shares of the REIT for additional liquidity. This conversion from OP Units to shares would trigger a tax liability.

Many real estate investors use the 721 Transaction to complement or as an alternative to Section 1031 Exchange. Real estate owners looking to invest in a more extensive portfolio with diversification, professional management, economies of scale, increased liquidity, and added estate planning benefits may find the REIT an attractive tool. The 721 Transaction can provide many benefits while deferring potential tax liability on their original property.

To execute a 721 Transaction investment property is contributed to the operating partnership of a REIT. Depending on the type of property the individual is contributing, it may be challenging to find a REIT willing to execute the UPREIT transaction. One may find it difficult to UPREIT a small apartment building, condo, or single-family home, as an example.

Many full-service real estate advisory firms, or sponsors, create investment programs to accommodate market demand for passive real estate 1031 exchange products. These programs, subject to the Securities Act of 1933 and investor suitability requirements, are often structured as Delaware Statutory Trusts (DSTs). Purchasing DST interests provide investors with a vehicle to exchange proceeds from a real property sale into professionally managed, institutional quality real estate through the Section 1031 Exchange process.

Many investors do not hold real estate attractive to a typical REIT for the UPREIT Transaction. Using the DST, an accredited investor sells tangible property to a third party and uses the proceeds from the sale to purchase a fractional interest in a DST. Following the 1031 guidelines, the investor would purchase interest equal to or greater than in the DST, potentially deferring any tax liability that may have been due.

The REIT can then acquire the DST asset through the UPREIT transaction. The operating partnership of the REIT is receiving all the DST interests from the beneficial owners in exchange for OP Units. By exchanging into a DST, an individual can access typical institutional assets attractive to a REIT.

Sometimes, these sponsors will create custom programs, where other registered entities they manage invest in the DST with a future option to purchase the investor ownership position. For example, imagine that an investment program sponsor creates both a publicly registered non-traded REIT and a DST program focused on the same type of asset. The REIT takes a percentage ownership position in the DST with the investor doing a 1031 exchange into the remaining position or mutually agreed to minority share. The REIT then has an option to purchase the investor interest in the future through the 721 UPREIT. A typical DST 721 Transaction should generally occur no less than two years after the beneficial owners acquire the DST interest. An agreement with a REIT, additionally, does not constitute a guarantee the REIT will execute the UPREIT transaction.

Further, should the REIT exercise its option to purchase the investor position in the DST, the investor may choose to accept OP units in the REIT through a Section 721 Exchange or as cash proceeds from the sale. Should the investor take the cash option, they can do another Section 1031 Exchange or keep the proceeds and pay taxes. Should the investor accept the OP Units in the REIT through the 721 Exchange, the investor may achieve greater diversification by owning the REIT.

Diversification

Many investors incur concentration risk by owning one property in a single market. REITs tend to own many assets diversified through different markets. The 721 Transaction into a REIT can give the ability to diversify an individual's portfolio, which may reduce concentration risk. A REIT can provide similar benefits of real estate ownership such as appreciation, tax shelter through depreciation, and income.

Income

Investors typically will receive income generated by the DST before a DST 721 Transaction and from OP Units of the REIT through distributions. Income generated by the DST or Op Units may have tax advantages due to depreciation and other strategies.

Liquidity

The ability to convert OP Units of the REIT to shares can provide liquidity benefits that are not standard with DST or property ownership. Partial or full liquidity may be achieved, depending on availability determined by the company, by converting the OP Units to shares of the REIT. While this is a taxable event, it gives more control to spread tax liability or access capital.

Estate Planning

A common estate plan is to pass real estate wealth on to the next generations. The 721 Transaction can be beneficial due to the increased liquidity provisions. There is often conflict on the division and timing of inherited assets within families and DST or real estate ownership can be restrictive on liquidity. On the other hand, ownership of OP Units converted to shares can split up how desired by the estate and can be passed to heirs at a step-up in basis, eliminating the potential tax liability due by the original owner upon passing.

Future Change to 1031 Tax Code

It is not unusual to see tax code overhauls with administration changes. The 2017 Tax Cuts and Jobs Act eliminated 1031 exchange for all assets besides real estate, and in the past year, legislative proposals have been made to further limit eligibility for 1031 exchanges. Proposed changes to Section 1031 are nothing new and will likely continue in the future. The 721 Transaction may be an attractive alternative to investors concerned about the prospect of restrictions on 1031 exchanges.

This is for informational purposes only, does not constitute as individual investment advice, and should not be relied upon as tax or legal advice nor does this informational material does not constitute an offer to purchase or sell securitized real estate investments. Please consult the appropriate professional regarding your individual circumstance. IRC Section 1031, IRC Section 1033 and IRC Section 721 are complex tax concepts, therefore you should consult your legal or tax professional regarding the specifics of your particular situation. Because investor situations and objectives vary this information is not intended to indicate suitability for any individual investor. There are material risks associated with investing in DST properties and real estate securities including liquidity, tenant vacancies, general market conditions and competition, lack of operating history, interest rate risks, the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short term leases associated with multi-family properties, financing risks, potential adverse tax consequences, general economic risks, development risks, long hold periods, and potential loss of the entire investment principal. Securities offered through Concorde Investment Services, LLC (CIS). Member FINRA/SIPC. Advisory services offered through Concorde Asset Management, LLC (CAM), an SEC registered investment advisor. Sequent Real Estate and Wealth Management is independent of CIS and CAM

The 1031 exchange is a powerful tool for investors in many industries, including agriculture. Agricultural land is an asset that can appreciate in value over time, and the 1031 exchange allows farmers and ranchers to defer capital gains taxes when selling and reinvesting in new properties.

The 1031 exchange, also known as a like-kind exchange, is a tax-deferred exchange that allows investors to sell an investment property and use the proceeds to purchase another similar property. This exchange enables investors to defer paying capital gains taxes on the sale, which can provide significant financial benefits over the long term.

For agricultural landowners, the 1031 exchange can be particularly valuable. Farmers and ranchers may own multiple parcels of land used for different purposes, such as grazing, crop production, or timber harvesting. Suppose they decide to sell one of these properties. In that case, they can use the proceeds to purchase a new property of equal or greater value while deferring the capital gains taxes that would typically be associated with the sale.

For exchange purposes, a like-kind replacement property means any property held for investment or business use. Following the 1031 Internal Revenue Code (IRC), farmland, vacant land, and certain agricultural assets can be exchanged for other real property investment assets.

If the owner lives in a house on the land, the house is considered the owner's personal property and would not be considered a like-kind exchange asset. Working with your tax and real estate advisors, the primary residence would be separated from the land, potentially taking advantage of IRC Section 121.

Another important consideration is the timing of the exchange. The IRS requires that the replacement property be identified within 45 days of the sale of the original property and that the purchase of the replacement property be completed within 180 days of the sale. This timeline can be challenging for farmers and ranchers who must carefully evaluate potential replacement properties before making a purchase.

Working with a qualified intermediary is essential when completing a 1031 exchange for agricultural properties. Intermediaries can help farmers and ranchers navigate the complex rules and regulations surrounding the exchange process and provide guidance on identifying and buying replacement properties.

To complete a successful Section 1031 tax-deferred exchange, the replacement property must be like-kind to the relinquished property. Some examples of like-kind properties include:

Any real estate held for productive use in a trade, business, or investment purposes is considered like-kind. A primary residence would not fall into this category; however, vacation homes or rental properties may qualify in some situations.

When executing a 1031 tax-deferred exchange, an investment property owner may find it challenging in today's market to locate suitable replacement property or maybe in their investment life cycle where they no longer want the day-to-day responsibilities of property management.

A Delaware Statutory Trust (DST) property ownership structure permits individuals to own a fractional interest in large, institutional quality, and professionally managed commercial property along with other investors, not as limited partners, but as individual owners within a Trust. A DST takes all decision-making out of the hands of investors and places it into the hands of an experienced sponsor-affiliated trustee.

When a taxpayer is interested in passive ownership of high-grade commercial property but lacks the financial wherewithal to purchase the property on their own entirely.

When the taxpayer wants a pre-packaged replacement property where the financing is in place and the sponsor has already performed due diligence.

As a reliable backup property on the list of identified properties in the event the primary specified property falls through or the taxpayer has not used all the proceeds from the sale of the relinquished property and wishes to reinvest the remaining funds to achieve full tax deferral.

In conclusion, the 1031 exchange can be a valuable tool for agricultural landowners looking to reinvest in new properties while deferring capital gains taxes. By carefully considering their options and working with a qualified intermediary, farmers, and ranchers can take advantage of the benefits of the 1031 exchange and continue to grow their agricultural businesses over the long term.

bd-eh-gp-a-1692-12-2023

© 2026 Sequent Real Estate + Wealth Management All Rights Reserved

A REIT is a security that sells like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages. REITs receive special tax considerations and typically offer investors high yields, as well as a highly liquid method of investing in real estate. There are risks associated with these types of investments and include but are not limited to the following: Typically no secondary market exists for the security listed above. Potential difficulty discerning between routine interest payments and principal repayment. Redemption price of a REIT may be worth more or less than the original price paid. Value of the shares in the trust will fluctuate with the portfolio of underlying real estate. Involves risks such as refinancing in the real estate industry, interest rates, availability of mortgage funds, operating expenses, cost of insurance, lease terminations, potential economic and regulatory changes. This is neither an offer to sell nor a solicitation or an offer to buy the securities described herein. The offering is made only by the Prospectus.Securities offered through Concorde Investment Services, LLC (CIS). Member FINRA/SIPC. Advisory services offered through Concorde Asset Management, LLC (CAM), an SEC registered investment advisor. Sequent Real Estate + Wealth Management is independent of CIS and CAM. Check the background of this firm on FINRA's BrokerCheck. To access Concorde’s Form Customer Relationship Summary (CRS), please click here. All information provided is for educational purposes only. The material contained herein does not constitute an offer to sell and is not an offer to buy real estate or securities. Such offers are made only by a sponsor's memorandum, which is always controlling and available to accredited investors only. There are material risks associated with the ownership of real estate, including but not limited to, tenant vacancies, loss of entire principal amount invested, and that potential cash flows, returns, and appreciation are not guaranteed. Past pricing structures may not be indicative of future pricing and may not result in positive returns.Securities offered through Concorde Investment Services, LLC (CIS). Member FINRA/SIPC. Advisory services offered through Concorde Asset Management, LLC (CAM), an SEC registered investment advisor. Sequent Real Estate + Wealth Management is independent of CIS and CAM. Check the background of this firm on FINRA's BrokerCheck. To access Concorde’s Form Customer Relationship Summary (CRS), please click here. All information provided is for educational purposes only. The material contained herein does not constitute an offer to sell and is not an offer to buy real estate or securities. Such offers are made only by a sponsor's memorandum, which is always controlling and available to accredited investors only. There are material risks associated with the ownership of real estate, including but not limited to, tenant vacancies, loss of entire principal amount invested, and that potential cash flows, returns, and appreciation are not guaranteed. Past pricing structures may not be indicative of future pricing and may not result in positive returns.

Sequent Real Estate + Wealth Management does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance.There are material risks associated with investing in DST properties and real estate securities including liquidity, tenant vacancies, general market conditions and competition, lack of operating history, interest rate risks, the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short term leases associated with multi-family properties, financing risks, potential adverse tax consequences, general economic risks, development risks, long hold periods, and potential loss of the entire investment principal. Past performance is not a guarantee of future results. Potential cash flow, returns and appreciation are not guaranteed. IRC Section 1031 is a complex tax concept; consult your legal or tax professional regarding the specifics of your particular situation. This is not a solicitation or an offer to sell any securities. DST 1031 properties are only available to accredited investors (typically have a $1 million net worth excluding primary residence or $200,000 income individually/$300,000 jointly of the last three years) and accredited entities only. If you are unsure if you are an accredited investor and/or an accredited entity please verify with your CPA and Attorney.

This site is published for residents of the United States only. Representatives may only conduct business with residents of the states and jurisdictions in which they are properly registered. Therefore, a response to a request for information may be delayed until appropriate registration is obtained or exemption from registration is determined. Not all of services referenced on this site are available in every state and through every advisor listed. For additional information, please contact Eric Scaff at escaff@sequent-rewm.com.